Home loan programs like FHA, VA, and USDA make it easier for buyers in Oregon and Washington to find financing that fits their needs. Each program has unique benefits, from zero-down options to flexible credit requirements. Here’s how to decide which one works best for you.

What’s the Difference Between FHA, VA, and USDA Loans?

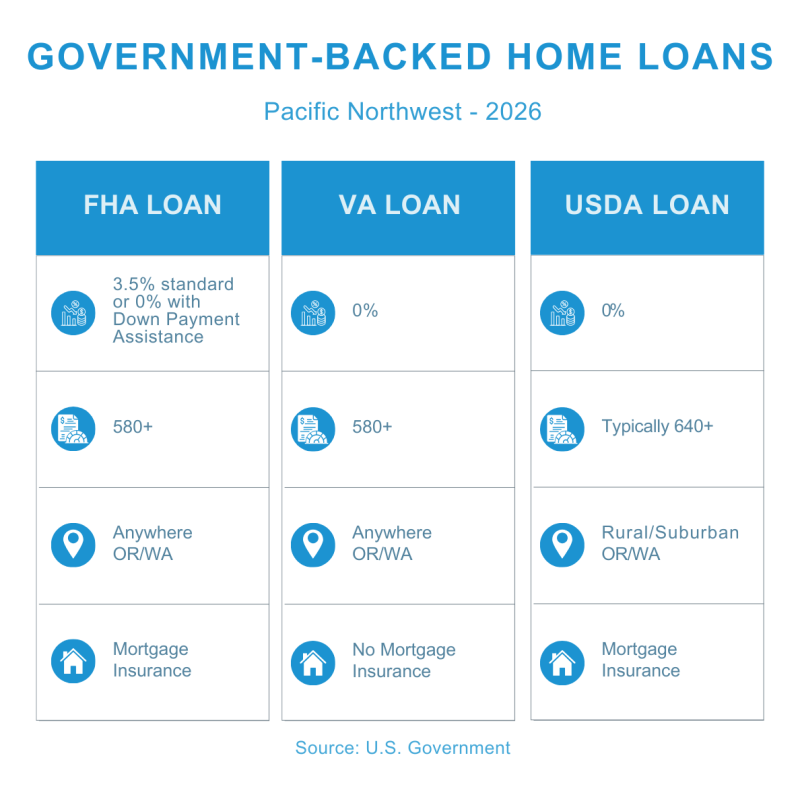

- FHA loans: Best for buyers with lower credit scores (at least 580). Available statewide in both Oregon and Washington.

- VA loans: Best for eligible veterans, active-duty service members, and surviving spouses. Offers 0% down payment with no monthly mortgage insurance.

- USDA loans: Best for buyers in qualifying rural and suburban areas who meet income limits. Offers 0% down payment for properties outside major metro areas.

Key differences at a glance:

|

Loan Type |

Down Payment |

Who Qualifies |

Location Rules |

|

FHA |

3.5% standard or 0% with Down Payment Assistance |

Most borrowers |

Anywhere in OR/WA |

|

VA |

0% |

Veterans and active military |

Anywhere in OR/WA |

|

USDA |

0% |

Income-qualified buyers |

Rural/suburban areas only |

The U.S. government backs these three popular mortgage programs to make homeownership more accessible. Each program serves different needs and comes with unique benefits and requirements.

If you’re struggling with down payment requirements or have been told you don’t qualify due to income restrictions or first-time buyer status, understanding these options becomes critical. Many Washington and Oregon residents don’t realize they may qualify for government-backed financing even if conventional loans seem out of reach.

The right choice depends on whether you have a military service history, where you want to live, your credit profile, and how much you can afford upfront. In the Pacific Northwest, where home prices have climbed significantly in cities like Seattle, Portland, and Bend, these programs can bridge the gap between renting and owning.

This guide breaks down exactly how FHA, VA, and USDA loans work in Oregon and Washington, what you need to qualify, and how to choose the best fit for your situation.

At a Glance: FHA vs. VA vs. USDA Loans

When you’re exploring government-backed mortgages in the Pacific Northwest, you’re looking at three main players: FHA, VA, and USDA loans. Each program is backed by a different federal agency—the Federal Housing Administration, the Department of Veterans Affairs, and the U.S. Department of Agriculture—and each serves a unique purpose in helping Americans achieve homeownership.

The beauty of these programs is that they tackle the biggest obstacles most buyers face: hefty down payments, strict credit requirements, and high monthly costs. But they each do it differently, and understanding these differences is the key to finding your best path forward.

|

Loan Type |

Minimum Down Payment |

Who It’s For |

Property Location Rules |

Mortgage Insurance/Fees |

|

FHA |

3.5% standard 0% with DPA |

Most borrowers with flexible credit |

Anywhere in OR/WA |

Upfront and annual MIP |

|

VA |

0% |

Veterans, active military, eligible spouses |

Anywhere in OR/WA |

One-time VA funding fee (no monthly insurance) |

|

USDA |

0% |

Income-qualified buyers |

Rural and suburban areas only |

Upfront and annual guarantee fee |

FHA loans: Flexible and accessible

FHA loans, insured by the Federal Housing Administration, help millions of Americans, especially first-time buyers, achieve homeownership. Here are some of the key benefits.

Low down payment

- 0% with Down Payment Assistance

- 3.5% down with a credit score of 580+

- 10% down with a credit score of 500–579

You can qualify with lower credit scores, which is ideal for rebuilding or establishing credit.

Wide availability

Available throughout Oregon and Washington for primary residences meeting FHA appraisal standards.

Mortgage insurance premium (MIP)

You’ll pay:

- Upfront premium: 1.75% of loan amount (can be rolled into loan) to keep upfront costs lower.

- Annual premium: Divided into monthly payments.

MIP protects the lender and typically remains for the life of the loan.

Learn more about how these loans work at FHA Loans.

VA loans: A benefit for service members

VA loans, guaranteed by the Department of Veterans Affairs, are designed for veterans, active-duty service members, and eligible surviving spouses. Here are the key benefits.

No down payment

Finance 100% of your home’s purchase price.

No monthly mortgage insurance

Saves tens of thousands of dollars over a 30-year mortgage compared with other low-down-payment loans.

VA funding fee

A one-time charge that:

- Can be rolled into your loan amount (no out-of-pocket payment at closing)

- Is waived for those receiving VA disability compensation

Certificate of Eligibility (COE)

This is required to prove you meet service requirements. We can help you obtain your COE.

Availability

Use your VA loan benefit anywhere in Oregon or Washington.

Find out more about your eligibility at our VA Loans page.

USDA loans: For rural and suburban development

USDA loans, guaranteed by the U.S. Department of Agriculture, promote homeownership in rural and suburban communities. Here are the key benefits.

No down payment

Finance 100% of your home’s purchase price.

Lower insurance costs

Guarantee fees are typically lower than FHA mortgage insurance.

Geographic restrictions

- Major urban centers (Seattle, Portland) don’t qualify

- Many suburban areas outside major cities do qualify

- Examples: Snohomish County, parts of Clark County, areas around Bend

We can help you check specific addresses on the USDA eligibility map.

Income limits

Based on location and household size. Designed for low- to moderate-income buyers, but limits are often generous, and many middle-class families qualify.

Guarantee fee

You’ll pay:

- Upfront: 1% (can be financed into loan)

- Annual: 0.35% (1/12th of 0.35% paid monthly)

Explore whether this program fits your situation at our USDA Loans page.

Finding your best fit

Each government-backed program serves different needs. The right choice depends on your unique situation—not which program is universally “best.”

Eligibility Deep Dive for FHA, VA, and USDA Loans in Oregon and Washington

Now that you understand what makes each loan type unique, let’s talk about whether you actually qualify. The truth is, FHA, VA, and USDA loans in Oregon and Washington each have their own specific requirements, and understanding these details can help you figure out which door is actually open to you.

Think of this section as your personal eligibility checklist. We’ll walk through credit scores, income requirements, property standards, and occupancy rules for each loan type, so you know exactly where you stand.

FHA loan requirements in OR and WA

FHA loans provide accessible financing for buyers with credit challenges or limited down payment savings.

Credit score requirements

- 580+: Qualify for 3.5% down payment

- 500–579: May qualify with 10% down payment

Note: Some lenders may require higher scores than the FHA minimums.

Down payment (3.5% minimum)

Acceptable sources:

- Personal savings

- Family gifts

- Down payment assistance programs. (We can help you with these.)

Debt-to-income (DTI) ratios

Standard guidelines:

- Housing payment (PITI): Under 31% of gross monthly income

- Total debt: Under 43% of gross monthly income

With strong compensating factors (cash reserves, solid payment history), approval is possible up to 55% DTI.

Loan limits

Loan limits in 2026 vary by county. Here are some examples for a single family residence:

- Lowest-cost areas: $541,828

- Highest-cost counties (King, Pierce, and Snohomish counties, WA): $1,063,750

Many counties fall somewhere in between. We can help you find the loan limit in the counties you are most interested in.

Property requirements

Property must be:

- Safe, sound, and secure

- Your primary residence (not for investment or vacation homes)

Basic requirements:

- Functioning roof

- Working plumbing and electrical systems

- No safety hazards

VA loan requirements for veterans in OR and WA

VA loans offer favorable mortgage terms for those who have served in the military.

Who qualifies:

- Veterans

- Active-duty personnel

- Reservists and National Guard members

- Certain surviving spouses

Service requirements:

- 90+ consecutive days of active duty during wartime, or

- 181+ days of active duty during peacetime

Certificate of Eligibility (COE)

Required to prove you meet the VA service requirements.

How to obtain:

- Through your lender

- Online via eBenefits portal

- By mail

We can help you obtain your COE.

Credit score

The VA doesn’t set a minimum credit score. Most lenders require 620 to 640, though lower scores may qualify through manual underwriting with a strong overall financial profile. Our requirement is lower than many at 580.

Residual income

The VA calculates how much money you’ll have left after paying major debts to ensure that you can comfortably afford:

- Food

- Utilities

- Other living expenses

This borrower-friendly approach goes beyond standard debt-to-income ratios. Many veterans can qualify for debt-to-income ratios higher than 60%.

Property requirements

Every property must pass a VA appraisal that verifies:

- Market value

- Minimum property requirements for safety, sanitation, and structural soundness

Occupancy requirements:

- Must be your primary residence

- Move in within 60 days of closing

- Exception: Spouse can fulfill requirement if service member is deployed

USDA loan requirements in OR and WA

USDA loans offer 100% financing for eligible properties in rural and suburban areas with no down payment required. USDA loans have more stringent requirements than FHA for income, debt-to-income ratios, and home location. But if you qualify, they can be valuable due to lower mortgage insurance rates and $0 down payment requirement.

Property location

- USDA-designated rural or eligible suburban areas

- Typically, communities with populations under 35,000

- Includes many suburban areas near Seattle, Portland, Spokane, and Eugene

We can help you check your specific addresses on the USDA eligibility site.

Income limits

- Designed for low- to moderate-income households

- Total household income cannot exceed 115% of area median income

- All adult household members’ income counts (even if not on the loan)

Examples: Income limits vary by county and household size (e.g., $90,000 to $110,000 for a family of four). We can help you check current limits on the USDA website for your county.

Down payment

Zero down payment with 100% financing available.

Credit score

Most lenders require 640+. The USDA doesn’t set a hard minimum—manual underwriting may be possible with lower scores and strong overall finances.

Property requirements

Must be:

- Single-family home

- Your primary residence

- Not designed for income-producing activities or working farms

USDA loans support residential homeownership, not commercial agricultural operations.

Finding the right fit

FHA, VA, and USDA loans each serve different buyer situations. Understanding eligibility requirements helps you choose the best option from the start.

Financial Breakdown: Costs, Fees, and Assistance

Let’s talk money. When you’re comparing FHA, VA, and USDA loans in Oregon and Washington, the down payment is just the beginning. Understanding the full picture of what you’ll pay upfront and over time—plus what help is available—can make a real difference in your budget and your decision.

Mortgage insurance and fees: FHA, VA, and USDA

Government-backed loans handle risk protection differently than conventional mortgages. Understanding these costs helps you evaluate long-term affordability.

FHA loans: Mortgage insurance premium (MIP)

Upfront MIP:

- 1.75% of the loan amount

- Can be rolled into the loan

Annual MIP:

- ~0.55% of the loan amount annually (can vary with loan term and down payment)

- Paid monthly (1/12th of the annual amount paid each month)

- Remains for the life of the loan (unless you make at least a 10% down payment)

VA loans: Funding fee

One-time fee at closing:

- Ranges from 1.25% to 3.3% of the loan amount

- Based on service category, prior VA loan use, and down payment amount

- Can typically be financed into the loan

- Waived for those receiving VA disability compensation

USDA loans: Guarantee fee

Upfront fee:

- 1% of the loan amount

- Can be financed into the loan

Annual fee:

Comparison with conventional loans

Conventional loans with less than 20% down require private mortgage insurance (PMI).

Key difference:

- PMI cancels once your loan is less than 78% of the original value when you financed your home.

- FHA MIP typically lasts for the life of the loan

Understanding these costs helps you compare what’s affordable upfront versus long-term.

Down payment assistance for FHA, VA, and USDA loans in Oregon and Washington

Down payment assistance (DPA) programs can reduce or eliminate the amount of money you need to bring to closing when combined with government-backed loans.

Washington state: Home Advantage program

Offered by: Washington State Housing Finance Commission

Assistance:

- Provides 3%, 4%, or 5% of the first mortgage loan amount

- Structured as a second mortgage

- Often features deferred payments and 0% interest rate

Combined with government or conventional loans:

- VA or USDA: 100% financing (zero money down) DPA helps with closing costs.

- FHA: Covers the down payment requirement and some closing costs.

- Conventional: Covers the down payment requirement and some closing costs.

Oregon: FirstHome program

Offered by: Oregon Housing and Community Services

Eligibility: Low- to moderate-income buyers

Assistance:

- Provides 4% or 5% of the first mortgage loan amount.

- Structured as a second mortgage.

- Can cover up to 100% of the cash requirement to close.

- Whether or not you have a payment on the second mortgage depends on your income level. We can help you understand this.

Combined with government or conventional loans:

- VA or USDA: 100% financing (zero money down) DPA helps with closing costs.

- FHA: Covers the down payment requirement and some closing costs.

- Conventional: Covers the down payment requirement and some closing costs.

How DPA programs work

Example scenarios:

- FHA loan (3.5% down): DPA covers the entire down payment and some closing costs.

- VA or USDA loan (no down payment): DPA covers closing costs (appraisal, title insurance, lender fees).

Benefits: Achieve homeownership without depleting your savings.

We’ve helped countless clients in the Pacific Northwest navigate these programs, and we know the ins and outs of combining them effectively. Every situation is unique, and we’re here to find the combination that works best for you. Learn more about down payment assistance options, or check out our frequently asked questions.

The bottom line? These programs exist to help you achieve homeownership, and we’re experts at making sure you take full advantage of every opportunity available to you.

Special Considerations for Pacific Northwest Homebuyers

Oregon and Washington have their own unique character, from the busy urban markets of Seattle and Portland to the peaceful rural landscapes of Eastern Washington and Southern Oregon.

When considering FHA, VA, and USDA loans in Oregon and Washington, there are specific factors that Pacific Northwest homebuyers should keep in mind, especially if you’re purchasing for the first time, building new construction, or trying to navigate the complexities of government-backed financing.

Benefits for first-time homebuyers in OR and WA

Government-backed loans help first-time buyers overcome common obstacles to homeownership in Oregon and Washington.

Low upfront costs

Down payment options that accelerate homeownership:

- FHA: 3.5% down or $0 with Down Payment Assistance

- VA and USDA: Zero down payment

- Conventional: As low as 3% down or $0 with Down Payment Assistance

Move from renting to owning sooner without needing years to save 20% down.

Flexible credit guidelines

Past financial challenges don’t automatically disqualify you. Government-backed programs offer more flexibility than conventional loans for buyers with imperfect credit.

Down payment assistance (DPA) programs

Oregon: FirstHome program

Washington: Home Advantage program

These programs can layer with FHA, VA, or USDA loans to potentially cover:

- Entire down payment

- Some closing costs

This means you can purchase your first home with little to no money out of pocket.

Homebuyer Education Courses

These are required by most DPA programs and some lenders. Different programs have different education requirements. Let us help you determine which education courses are best for you.

What you’ll learn:

- Homebuying process

- Budgeting strategies

- Maintenance responsibilities

- Investment protection

These courses help you make informed, confident decisions about your first home purchase.

Why work with a local mortgage professional

Navigating government guidelines, state programs, county loan limits, and property eligibility requirements is complex. A local mortgage professional simplifies the process.

State-specific program expertise

We understand Oregon’s FirstHome and Washington’s Home Advantage programs thoroughly:

- Quickly assess your eligibility.

- Identify the best program combinations.

- Ensure that you maximize the available benefits.

- Provide current, accurate information on changing requirements.

Local market knowledge

We bring expertise that national call centers and online-only lenders can’t match:

- Growth patterns in Seattle, Portland, Spokane, Eugene, and Bend

- Rural markets in Eastern Oregon and Washington

- USDA property eligibility by area

- FHA loan limits by county

Access to multiple lenders

We shop your scenario to find excellent rates and terms:

- Not all lenders offer all programs.

- Competitiveness varies by borrower situation.

- We handle the comparison work.

Compliance and documentation

We ensure smooth transactions by:

- Verifying complete and accurate documentation

- Confirming that properties meet FHA, VA, or USDA appraisal standards

- Managing requirements when combining government loans with DPA programs

Streamlined process

We act as your advocate and coordinator:

- Communicate with real estate agents, appraisers, title companies, and underwriters.

- Translate complex mortgage terms into plain language.

- Anticipate and prevent potential issues.

Our goal

Our goal is to make your journey to homeownership in Oregon and Washington smooth, stress-free, and successful—whether you’re a first-time buyer, a veteran, or are seeking a home in a rural community.

Frequently Asked Questions

You’ve made it this far, which means you’re serious about exploring your mortgage options. We love that! Now let’s tackle some of the most common questions we hear from homebuyers considering FHA, VA, and USDA loans in Oregon and Washington.

What are the 2025 FHA loan limits in Oregon and Washington?

Here’s something that surprises many people: FHA loan limits aren’t a one-size-fits-all number. They’re set by HUD and vary significantly from county to county, reflecting the reality that a home in rural Walla Walla costs quite a bit less than one in downtown Seattle.

For 2026, the lowest FHA loan limit for single-family home loans sits at $541,828. This is the baseline limit applied across most low-cost counties in both Oregon and Washington.

But in high-cost areas—we’re talking places like King County—the FHA ceiling jumps all the way up to $1,063,750 for single-family home loans. That’s a substantial difference that can make a real impact on what you can afford in these competitive markets.

Always ask us to check the specific loan limits for the county where you’re planning to buy. Even neighboring counties can have different limits. We can look this up for you in seconds and make sure you know exactly what your purchasing power looks like in your desired location.

Which mortgage program is best for Oregon or Washington homebuyers?

The best mortgage program depends on your situation. Choose a VA loan if you’re an eligible veteran or active-duty service member. This loan offers 0% down with no monthly mortgage insurance, providing the most favorable terms available.

An FHA loan can help if you have a lower credit score (580+) or limited savings, as it requires just 3.5% down and has flexible credit requirements available statewide.

Opt for a USDA loan if you’re buying in a qualifying rural or suburban area and meet income limits—it offers 0% down payment for properties outside major metro areas.

Let us help you find the right loan.

Many Oregon and Washington homebuyers can also combine these programs with state down payment assistance (Oregon’s FirstHome or Washington’s Home Advantage) to cover closing costs and reduce out-of-pocket expenses even further. The right choice depends on your military service history, credit profile, where you want to live, and how much you can afford upfront.

How do I check if a property is in a USDA-eligible area?

Many homebuyers assume USDA loans are only for remote farmland, but that’s simply not true. A significant number of suburban communities—even those within commuting distance of Seattle, Portland, and Spokane—actually qualify.

The easiest and most accurate way to check is using the official USDA Eligibility website. You can enter a specific property address to get a definitive yes-or-no answer, or you can browse the interactive map to explore eligible areas. The USDA’s definition of “rural” is surprisingly generous, typically including communities with populations under 35,000.

We encourage you to play around with the USDA Eligibility Site or contact our team before you start house-hunting. You might find that your dream neighborhood is USDA-eligible, opening up financing options you didn’t realize you had.

What is a Certificate of Eligibility (COE) for a VA loan, and how do I get one?

If you’re a veteran, active-duty service member, or eligible surviving spouse, your Certificate of Eligibility (COE) is your golden ticket to accessing the incredible benefits of a VA loan. Let’s break down what it is and how to get your hands on one.

What it is: The COE is an official document from the Department of Veterans Affairs that proves to mortgage lenders that you meet the military service requirements for a VA-backed home loan. It confirms your entitlement to the VA home loan benefit based on your service history.

Important note: Having a COE doesn’t guarantee loan approval—that still depends on your credit, income, and other factors—but it’s an essential first step.

How to get one: You have three main options, and honestly, the first one is the easiest:

- Through a lender like us. This is by far the most common and fastest method. We have direct access to the VA’s online portal and can often retrieve your COE instantly while you’re sitting in our office or during a phone call. No waiting, no hassle.

- Online via the eBenefits portal. If you already have an eBenefits account set up, you can log in yourself and apply for your COE directly. It’s a straightforward process if you’re comfortable navigating government websites.

- By mail. You can complete VA Form 26-1880, “Request for Certificate of Eligibility,” and send it to the appropriate VA regional loan center. This is the slowest option, but it works if you prefer paper applications.

We typically handle the COE retrieval for our clients because it speeds up the entire VA loan application process. There’s one less thing for you to worry about, and you get to focus on finding your perfect Pacific Northwest home.

Find Your Path to Homeownership in the Pacific Northwest

After exploring FHA, VA, and USDA loans in Oregon and Washington, you have a clearer picture of options beyond conventional mortgages.

Which loan fits your situation?

FHA loans

- Best for buyers with credit challenges

- 3.5% down payment available or eligible for DPA

- Need for flexible credit guidelines

- Down payment assistance often eliminates the need to save for a down payment

VA loans

- Veterans, active-duty service members, Reservists and National Guard members and certain surviving spouses

- 0% down payment

- No monthly mortgage insurance

USDA loans

- Best for buyers seeking properties in eligible rural/suburban areas

- 0% down payment

- Lower-cost markets outside major cities

Making homeownership accessible

Government-backed programs help when conventional loans seem out of reach. Combined with down payment assistance, many Pacific Northwest families achieve homeownership with minimal out-of-pocket expenses.

We’re here to help

We specialize in government-backed loans for Oregon and Washington residents:

- Washington’s Home Advantage program

- Oregon’s FirstHome program

- County-specific FHA loan limits

- USDA neighborhood eligibility

- VA benefit navigation

You don’t have to figure this out alone. Explore your loan program options, and let us help you navigate them and turn your homeownership goal into reality.

Resources